Alumni and Tuck Faculty Join In Study of Stock Ownership

ASSISTANT PROFESSOR OF BUSINESS ADMINISTRATION

ALUMNI from New York City, other New York businessmen, and Tuck School faculty members have joined in a new cooperative undertaking - the Dartmouth Economic Research Council. Financed and encouraged by the Committee for Economic Development, the Dartmouth Council will operate for three years, investigating whatever topics it thinks are worthy of its time and effort. The first subject chosen is "Broadening the Basis of Stock Ownership."

The long-range objectives of the Council are:

1. Enlisting the loyalty and enthusiasm of its alumni in an important educational undertaking.

2. Promoting cooperative and mutually beneficial relations between the Dartmouth faculty and members of the business and financial community.

3. Encouraging businessmen to take an interest in, and devote time to, the study of economic affairs so as to develop findings and recommendations for business and public policy which will contribute to the preservation and strengthening of our free society.

4. Bringing about increased public understanding of the importance of these objectives and the ways in which they can be achieved.

With Professor John Griswold as hairman, and Professors Kenneth Davis and Marshall Robinson as members, a Tuck School faculty advisory committee and a group of alumni chose the initial topic. The alumni advisers were C. E. Brundage '16, H. R. Campbell '21, O. H. Hicks '21, J. P. Merriam '31, P. B. Merry '26, H. W. Newell '20, W. M. Sayre '37 and J. C. VanderPyl '10.

Three economic considerations make "Broadening the Basis of Stock Ownership" important. First, what are the implications of the changing pattern of distribution of income in the United States?

In the past fifteen to twenty years the number of families and individuals in the middle income ranges has increased markedly while the percentage share of family personal income going to the top 20% of income receivers has declined. For example, only about one million, or 3% of consumer units, were in the $5,000 and over bracket in 1935-36, whereas in 1950 some 14 million, or almost 30% of the total, had incomes of $5,000 or more (earnings before income taxes in both cases). The upward shift is present whether incomes are expressed in constant dollar figures or in current dollars. Over the same period the percentage share of family personal income received by the highest 20% of families ranked by size of income has declined by about 15%, and that received by the top 5% (average income in 1950 about $19,500) has declined by about 27%.

The significance of these changes in income for stock ownership is a matter of controversy. One recent study concluded that the upper income group, despite inroads made by taxation, still has the largest amount of savings and therefore the largest investment potential. On the other hand, President Keith Funston of the New York Stock Exchange holds that people of moderate means now provide and will increasingly in the future provide the market for common stocks. His argument rests in part on an estimate which states that three out of four shareholders in the United States have incomes below |10,000. In 1953 and 1954 individual investors with incomes under $10,000 provided as much activity on the Exchange as those in the $10,000 to $25,000 bracket and those with incomes above $25,000. It appears that the question of where is the market for stocks is still open.

If the middle income group should be called on to provide the bulk or a large portion of capital funds in the future, then the implications of this for the people involved cannot be ignored. What are the attitudes, goals, and aims of individuals who participate in installment plans to buy stock? What is the effect on their financial position of changes in stock prices? What is the structure of their assets and what are their savings habits?

The second consideration is how should the savings of individuals be channeled to supply the capital needs of an expanding economy?

Since the close of World War II, stock financing has contributed about 7% of the total of over 200 billion dollars in new corporate funds. For every dollar raised by new stock issues industry has gone into debt more than $3 and supplied more than $9 from retained earnings and depreciation reserves. Of course, current savings of individuals flow into financial institutions such as banks and savings and loan associations, private life insurance companies, pension funds and investment companies and may in turn be invested in corporate stock by the financial institutions. However, equity holdings and purchases of these financial institutions as a group are dwarfed by the amount of debt capital which they supply to the economy. As of the end of 1953 their total assets were estimated at 122 billion dollars while equity holdings were 10 billions. Examples of questions which need to be explored are the different effects of financing expansion through retained earnings as compared to seeking new funds in the market, and the dangers, if any, to the country of the heavy reliance on debt financing.

The third consideration is the controversial issue of "who owns the corporations" the giant units under whose aegis a major share of production of goods takes place. Companies frequently state in annual reports and in institutional advertisements the total number of their shareholders, and view large numbers with pride. This widespread ownership can also be viewed with alarm, as in the fear that "Wall Street" controls the country, or as a matter of no practical concern. The U. S. National Resources Committee has stated that "in practice, ownership of most large corporations has become so dispersed that the stockholders have ceased to be able to exercise a very significant degree of control over corporate policy." The Dartmouth research committee will explore such questions as: Is the stockholder interested in the affairs of the corporations he owns? Does his stock ownership contribute to his understanding of our economic system? Will widened ownership influence the direction of corporate activity in any way? What is the strength and meaning of the idea of "Wall Street" control of business?

To carry out its work the group is organized into three components: (1) TheBusiness Advisory Committee, consisting of top executives in the New York City business and financial world. This group assists in planning the research projects, selects the members of the Business Executives Research Committee, and acts in a general advisory capacity. (2) The Business Executives Research Committee, consisting of executives who already occupy important positions in their firms and are destined to assume greater responsibility in the future. The BERC is the "working group" which, together with the College Advisory Committee, carries on the actual research. (3) The College Advisory Committee, consisting of staff members of the Tuck School and including a research coordinator. This group serves in an advisory capacity and makes available to the BERC the resources of Dartmouth College and its faculty.

Alumni members of these committees are:

BUSINESS ADVISORY COMMITTEE A. E. Allen '32 K. W. Fraser '31 B. V. Brooks Jr. '47 O. H. Hicks '21 C. E. Brundage '16 C. Kellogg '28 G. H. Chamberlaine '21 S. S. Larmon '14 G. T. Conklin Jr. '36 R. L. Loeb'21 C. W. DeMond '19 C. F. McGoughran '20 Sumner Emerson '17 Kirt Meyer '30 J. C. Fell! '20 C. E. Newton '20 A. F. Flouton '36 H. W. Wilson '18

BUSINESS EXECUTIVES RESEARCH COMMITTEE R. A. Allen '46 R. P. Fisher '45 A. Bullock '46 T. J. Mullen '49 D. E. Cummings T'50 E. M. O'Brien T'50 G. N. Farrand '33 R. E. Rooke '49 G. J. Ferrarese '47 H. C. Whiteman '50 R. E. Field '43 S. C. Williams '40

The Executive Committee of the New York group - Chairman Charles McGoughran, and B. V. Brooks Jr., G. H. Chamberlaine, and Orton H. Hicks - has done important work in defining the scope and method of research of the topic. At the "kick-off" dinner, held on October 28, Chairman McGoughran established direction for the project in his talk on the benefits to the business community of broadening the base of stock ownership. He pointed out that a wider stock ownership will make the individual a part owner of American industry and thereby contribute to his better citizenship. He also discussed the issue of the small saver as a principal source of funds in the capital market.

In carrying out the research effort, the working committee is broken down into groups of six, each to work on a sub-topic of its own choosing. Chairmen of the research groups include Richard A. Allen T'50; Edward M. O'Brien T'50; and Arthur Bullock T'50. These men are key participants in the project for they must keep the work of the research groups progressing and must take an active part in the preparation of preliminary reports.

The close association of alumni and the College is frequently talked about as a virtue. Here is a practical way of enlisting cooperation and building up such association in a venture that may bring important results to a wider group. The task has begun successfully, to the benefit of those who are actively participating, and we look forward to a worthwhile conclusion through a sound investigation of an important topic.

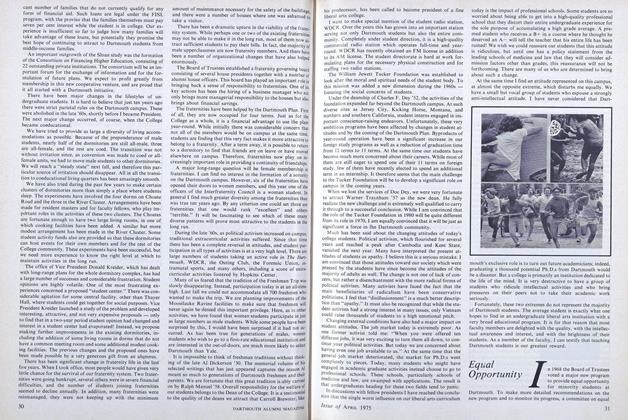

A New York meeting of the executive committee of the Dartmouth Economic ResearchCouncil. Left to right, seated: B. V. Brooks Jr. '47, Charles F. McGoughran '20, GeorgeH. Chamberlaine '21 and Orton H. Hicks '21. Standing: H. W. Newell '20, who died onDecember 19, Prof. James P. Logan, the author of this article, Robert Donaldson, andProf. John A. Griswold of Tuck School.