More Bone and Sinew For a Growing College

"...and that the said Corporation .. .shall be able and in law capable . . . to haveaccept and receive any rents profits annuities gifts legacies donations or bequestsof any kind whatsoever..."

So READS a section of the Charter of Dartmouth College issued on the 18th day of December 1769 under the seal of "George the Third by the grace of God of Great Britain France and Ireland King Defender of the Faith, and so forth."

And fortunate it was that the Corporation (The Trustees of Dartmouth College) was empowered to accept and receive legacies and bequests, for a large share of the capital funds of the College presently functioning as endowment was received from these sources.

The story of these benefactions as recorded by Halsey Edgerton '06 in a compilation published in 1940 is an inspiring one. Arranged alphabetically, it begins with a note concerning a legacy by Mrs. Edith M. Abbott of Middlebury, Vt., widow of Charles Abbott of the Class of 1891, recording receipt of $500 to "The Alumni Fund of Dartmouth Cqllege ... to be credited to the Class of '91," and ends with record of a legacy of $300 by Henry D. Wyatt of the Class of 1871 with "no condition or restriction."

Between the bare bones of these factual recitals, one may, with a little imagination and reading between the lines, piece together a story of devotion, sacrifice and faith in the heritage and destiny of Dartmouth College that is "altogether heartwarming. Here are the names of Dartmouth's great benefactors, Baker, Bommer, Brown, Bullard, Carpenter, Chandler, Cohen, Cummings, Fayerweather, Hall, Hayes, McNutt, Otis, Parkhurst, Pike, Sage, Salter, Sanborn, Silsby, Steele, Topliff, Town, Tuck, Ward, Wentworth and others who have given substantial sums to the cause of liberal arts education. But here also are all the names of those benefactors whose numerous lesser gifts, in total, approach the total of the larger gifts.

Here, truly, is the record of the accumulation of the treasure, the very bone and sinew, that has made possible Dartmouth College as we know it today. Whether the gift has been for endowment of a scholarship, for faculty salaries, for a building, for the library, for "the installation of colonial street lamps" or "without condition or restriction," all have contributed and will continue over the years to contribute to building an ever greater Dartmouth College.

It is therefore altogether fitting that the Development Council and Trustees, in declining to embark upon a so-called "high pressure" campaign to add immediately to Dartmouth's capital fund, are relying heavily on a bequests program to make vitally necessary increases in endowment over a period of years. The bequests program, now being organized and directed by the Alumni Council Committee on Bequests has become an integral part of the over-all program announced by the chairman of the Development Council, H. R. Lane '07 of Boston. It becomes a major segment of an integrated program which will build a greater Dartmouth. The Alumni Fund will continue to solicit annual gifts for current use. The Class Memorial Funds will continue to be the mechanism for each class to make a group capital gift to the College on the occasion of its 35th reunion. The bequests program will provide the opportunity for all, so minded, to include the College in their estate planning.

The foundations for the present program were laid by previous Committees on Bequests under the leadership of Roswell F. Magill '16, Arthur S. Dunning '11, and John L. Sullivan 'si. It remained, however, for the formulation of the over-all program by the Development Council to provide the impetus for a general appeal. Within the framework of the whole plan, the Committee on Bequests has now proposed, and the Alumni Council has approved, a frank approach to individual members of all classes past their 25th reunion to suggest that each man make some provision for Dartmouth College in planning the disposition of his estate. Bequests from others will be welcome, as always, but in order to avoid encroachment into the field of the Memorial Funds, active efforts to encourage bequests will be confined to post-25th reunion classes.

These approaches, for the most part, will be made by individual class committees, assisted whenever necessary by members of the staff in Hanover. Moreover, realizing the legal and technical problems which will inevitably arise in many individual cases, the aid of Dartmouth lawyers has been enlisted. It is expected that in most cases prospective donors will consult their own lawyers for advice in connection with the formulation and execution of any plan for the disposition of their estates. In any case where the donor may request assistance, however, the Committee expects to be able to assist in obtaining expert legal advice.

Ten classes which have had reunions during the past two years have taken formal action in support of the bequests program and many have appointed class chairmen to organize the work. Many other post-25th reunion classes have or are currently appointing bequests chairmen and proceeding with the program.

The approach to individuals will be aimed, first, to encourage each to make some provision for the College, and second, to explore with each who may be willing to do so, the methods by which advantage may be taken of certain provisions of the tax laws which make it possible to make generous gifts to the College while at the same time safeguarding and protecting the interests of dependents.

It is quite generally known, in a vague fashion, that certain tax deductions and exemptions are available to the donor in the case of gifts and bequests to educational institutions. The extent to which governmental tax policies favor such gifts is not generally realized, however.

Very few understand, for example, that by setting up a testamentary trust in which the College receives the assets of an estate only after the death of beneficiaries who are to receive the income during their lifetime, estate taxes are materially reduced because only the value of the life interest, calculated on the life expectancy of the beneficiaries at the date of the death of the creator of the trust, is subject to tax. The principal, on demise of the beneficiaries, passes to the College without further tax. Because of this reduction in estate taxes, the beneficiaries of such a trust willfrequently receive a larger income than ifthe estate had been left outright to them.

One of the first tasks of the Committee has been the preparation of a booklet entitled Philanthropic Estate Planning which explains many aspects of the tax laws in relation to gifts and bequests to educational institutions. Initially a small edition was distributed last summer to Dartmouth lawyers and bankers for comment and suggestion, and since that time additional copies have been printed for more general distribution. Copies are available on request to Ross Gamble, Secretary, Committee on Bequests, Crosby Hall, Hanover, New Hampshire.

In the preparation of the booklet, and in the study of this entire problem, it has become increasingly clear to the Committee that in many cases philanthropic gifts made during one's lifetime may have substantial tax advantages which will fail to accrue in the case of a testamentary gift. For this reason the Committee has found it necessary, in its thinking and planning, to think of the term "bequests" not in the limited sense of testamentary gifts only, but in a larger and perhaps not strictly accurate sense which includes gifts in the nature of or in anticipation of bequests. Thus, we include life insurance in which the College is named as beneficiary, gifts subject to reservation of life income, gifts subject to reservation of annuity, and living trusts.

Little need be said regarding life insurance except to point out that if the College is named as irrevocable beneficiary, premiums paid thereafter are deductible as a charitable gift for income tax purposes. Moreover, the fair value of the policy is deductible in the year in which the College is designated irrevocable beneficiary. It is expected that these tax features may be attractive to many men whose need for insurance has decreased as their children have reached maturity.

In this area of gifts in anticipation of bequests, it is also expected that gifts subject to reservation of life income or subject to reservation of annuity may offer attractive possibilities to many. Gifts of this type deserve a special word because they represent a new departure in the announced financial policy of the College.

The College is now prepared to accept a gift subject to reservation of life income and to undertake to pay to the donor, or to one person designated by the donor, or to one person and upon the demise of that person to a designated survivor, a return based on the average net rate of return earned by the College on its pooled invested assets. The donor obtains the benefit of a diversified investment program under expert supervision. In addition, a substantial portion of the gift is considered to be a tax-free donation, and is deductible for income tax purposes. In many cases this produces important results. For example, if a donor at age 60 gives $5000 to the College and reserves a life income to himself, the gift portion available for income tax reduction will be $2997. If the donor be assumed to have a net income of approximately $25,000, his highest effective tax rate will be about 60% (for an individual filing a separate return). His income tax will, therefore, be reduced by $1798, so that his $5000 gift will cost him only $3201 net. Assuming now that the average rate of return earned by the College on its pooled invested assets is 4.4% for a given year, the donor would receive an income of $220 for that year. Based on the net cost of the gift, however, the donor would receive a return of better than 6.8%.

The College is also prepared to accept a gift subject to reservation of annuity and to undertake to pay to the donor, or to the donor and one other, an annuity at certain specified rates. These rates are lower than those offered by representative insurance companies; but the differential is partly, and in some cases wholly, offset by the fact that a portion of the gift is deductible for income tax purposes in the year in which the gift is made.

Another aspect which frequently offers important advantages to the donor is the treatment, under the tax laws, of securities or other property which have been held for at least six months and have appreciated in value. Long term capital gains are taxed at 25%. But if property which has appreciated in value is given to the College, the gift is valued as a deductible contribution at its current market value withno capital gain tax assessed against theappreciation.

The results, in many cases, are spectacular. For example, consider the case of a donor owning securities which cost $2500 and have a present market value of $5000. In the hands of the donor, after deducting a capital gains tax of 25% or $625, the securities have a net value of $4375. If, however, he gives these securities to Dartmouth College, and if his net income for the year is over $28,000, his income tax (for an individual filing a separate return) will be reduced by $3,450 and his gift of $5000 to the College will cost him only $925 net. The higher the income of the donor, of course, the greater the tax saving.

Applying this principle to gifts subject to reservation of life income or to reservation of annuity will obviously increase the advantages of those methods of giving for those who own property which has appreciated in value. Thus, in the above case, if the gift were made subject to reservation of life income, and if again, the College rate of return is assumed to be 4.4%, the rate of return to the donor based on the net cost of the gift would be 23-7%-

There are many other attractive opportunities for tax savings in particular situa tions. But in pointing out these possibilities, it should be emphasized that we are not suggesting tax evasion, nor are we suggesting that potential donors take advantage of "loopholes" in the tax laws. The provisions we mention are not loopholes, and accepting the deductions permitted by these provisions is not tax evasion. These are provisions which have been consciously and intentionally written into the tax laws for the specific purpose of encouraging charitable gifts.

A Dartmouth alumnus, John Pearson 'ii, published an article entitled "Death and Taxes" (Atlantic Monthly, May 1949) describing the devastating effects of estate and inheritance taxes on large estates. He cited the case of W. K. Vanderbilt whose $35,000,000 estate dwindled to $5,000,000 after taxes. Mr. Pearson sought an answer to the question why so many persons fail to take advantage of tax encouragement of a philanthropic distribution of property. He came to the conclusion that while there may be many contributing causes, a major cause was unquestionably a lack of understanding or sheer ignorance of the workings of the tax laws.

One of the tasks of the Committee on Bequests, therefore, will be to try to increase the understanding of Dartmouth alumni and friends of the College on this subject. Obviously it is the business of a Committee on Bequests to promote the idea of bequests to the College, using the term "bequests" in the larger sense as defined above. Less obviously, this Committee will make it its business to try to show prospective donors how they may make gifts to best advantage.

To this end we ask for your patience, cooperation and understanding. When you are approached by your class chairman, you may be inclined to say: "I can't afford it." If you will give him a chance, you may be surprised to discover the small cost of a sizable gift to the College.

Above all, in these approaches, we will respect your personal privacy. All class chairmen and others having to do with this program will be requested to refrain from inquiry into your private affairs.

It will not be possible, however, to suggest specific methods of tax saving unless certain facts are available for analysis. We hope that many individuals may offer to supply the necessary facts for that purpose. Any information supplied will be treated in the strictest confidence.

The Committee recognizes that the disposition of one's estate is a serious, indeed a solemn, business. We, and the officers and staff of the College, propose to approach our task in that manner. We now suggest merely that you give this program your thoughtful consideration, recognizing that there are few causes which so justly merit your support, and that there are few institutions in which you may erect so enduring a monument.

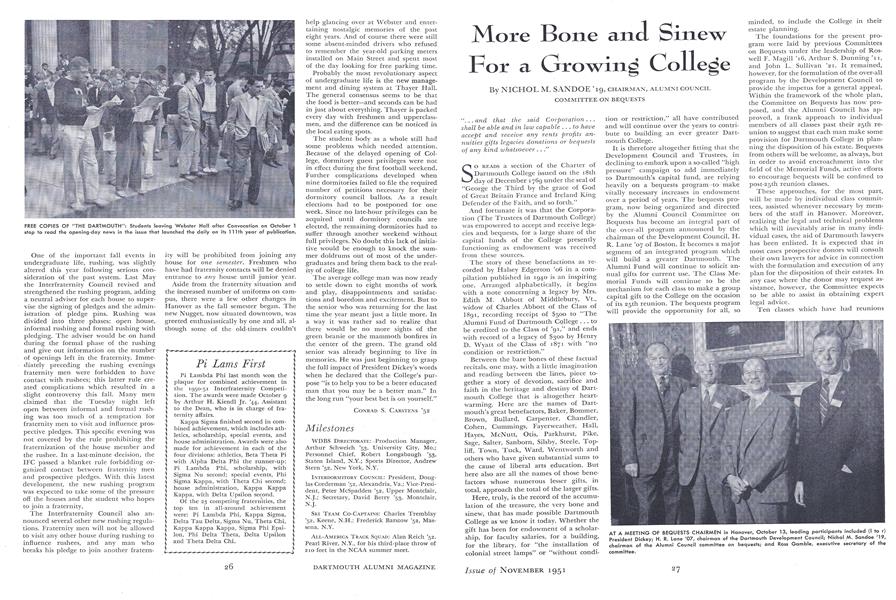

AT A MEETING OF BEQUESTS CHAIRMEN in Hanover, October 13, leading participants included (I to r) President Dickey; H. R. Lane 'O7, chairman of the Dartmouth Development Council; Nichol M. Sandoe 'l9, chairman of the Alumni Council committee on bequests; and Ross Gamble, executive secretary of the committee.

ALUMNI COUNCIL MEMBER: Francis Brown '25, editor of "The New York Times Book Review," who was elected member-at-large at the June meeting of the Council. He is also newly elected to the Advisory Board of the "Dartmouth Alumni Magazine."

NEW ADDRESS? If you have moved or are about to move, please notify the ALUMNI MAGA-ZINE immediately. To get the next issue to you, we must know your correct ad- dress by the 10th of the month. Be sure to include your zone number.

CHAIRMAN, ALUMNI COUNCIL COMMITTEE ON BEQUESTS