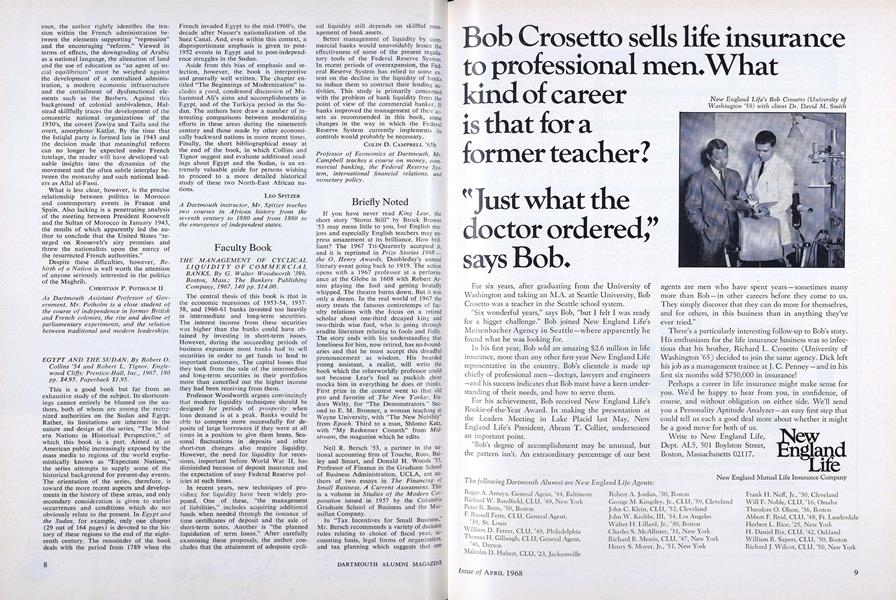

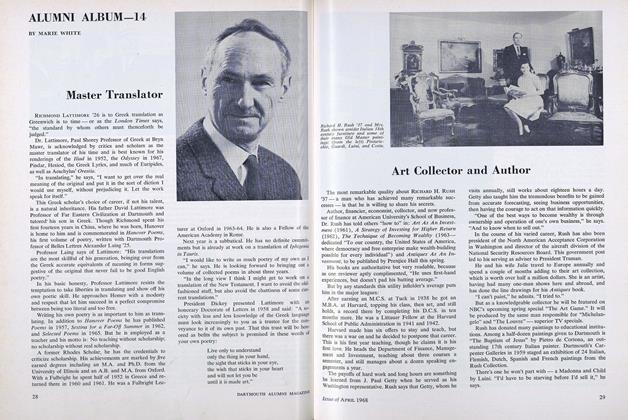

THE MANAGEMENT OF CYCLICAL LIQUIDITY OF COMMERCIAL BANKS.

By G. Walter Woodworth '39h.Boston, Mass.: The Bankers PublishingCompany, 1967. 140 pp. $14.00.

The central thesis of this book is that in the economic recessions of 1953-54, 1957-58, and 1960-61 banks invested too heavily in intermediate and long-term securities. The interest income from these securities was higher than the banks could have obtained by investing in short-term issues. However, during the succeeding periods of business expansion most banks had to sell securities in order to get funds to lend to important customers. The capital losses that they took from the sale of the intermediate and long-term securities in their portfolios more than cancelled out the higher income they had been receiving from them.

Professor Woodworth argues convincingly that modern liquidity techniques should be designed for periods of prosperity when loan demand is at a peak. Banks would be able to compete more successfully for deposits of large borrowers if they were at all times in a position to give them loans. Seasonal fluctuations in deposits and other short-run changes also require liquidity. However, the need for liquidity for recessions, important before World War 11, has diminished because of deposit insurance and the expectation of easy Federal Reserve policies at such times.

In recent years, new techniques of providing for liquidity have been widely proposed. One of these, "the management of liabilities," includes acquiring additional funds when needed through the issuance of time certificates of deposit and the sale of short-term notes. Another is "the planned liquidation of term loans." After carefully examining these proposals, the author concludes that the attainment of adequate cyclical liquidity still depends on skillful management of bank assets.

Better management of liquidity by commercial banks would unavoidably lessen the effectiveness of some of the present regulatory tools of the Federal Reserve System. In recent periods of overexpansion, the Federal Reserve System has relied to some extent on the decline in the liquidity of banks to induce them to contract their lending activities. This study is primarily concerned with the problem of bank liquidity from the point of view of the commercial banker. If banks improved the management of their assets as recommended in this book, some changes in the way in which the Federal Reserve System currently implements its controls would probably be necessary.

Professor of Economics at Dartmouth, Mr.Campbell teaches a course on money, commercialbanking, the Federal Reserve System,international financial relations, andmonetary policy.

Books

-

Books

BooksAlbert W. Levi '32, is the author

December 1933 -

Books

BooksELEMENTARY COLLEGE PHYSICS

May 1937 -

Books

BooksIDEAS, WEALS, AND AMERICAN DIPLOMACY: A HISTORY OF THEIR GROWTH AND INTERACTION.

OCTOBER 1966 -

Books

BooksGRAMATICA ESPANOLA DE REPASO.

July 1958 -

Books

BooksA CRITICAL INTRODUCTION TO ETHICS,

April 1949 -

Books

Books"This Land Is My Land ..."

APRIL 1984